How to Protect Assets from Nursing Home Costs in Florida: A 2026 Senior Guide

- dcjrichards

- May 27

- 7 min read

Updated: Jun 4

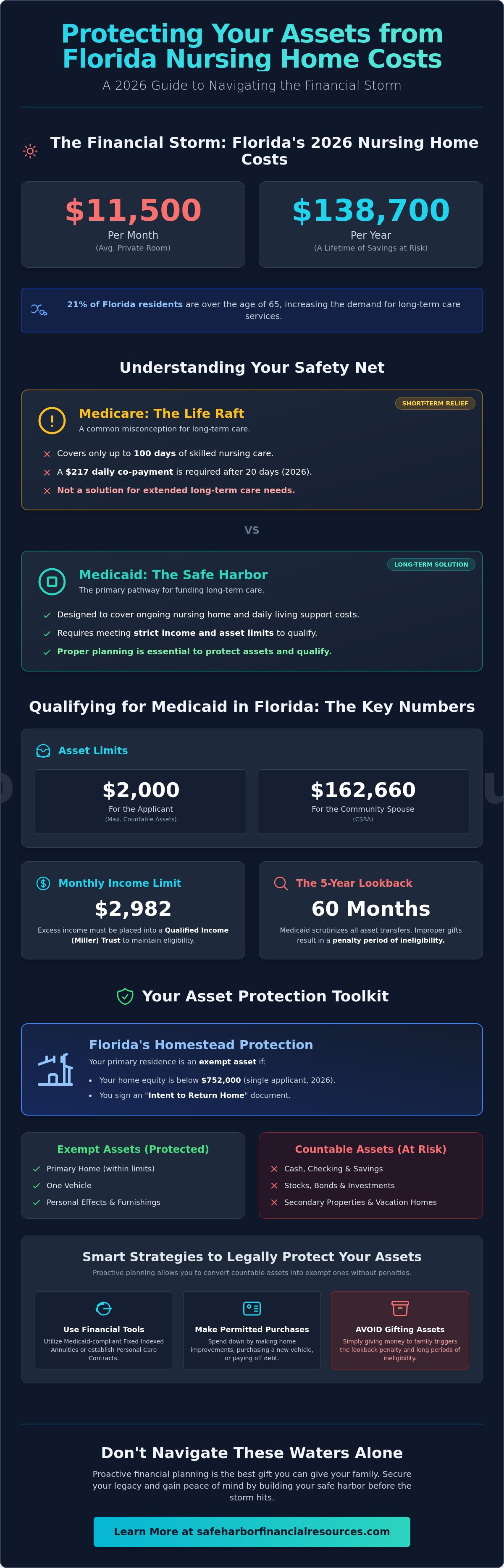

With the average cost of a private room in a Florida nursing home reaching $11,500 every single month in 2026, many families in Palm Beach County feel like they're sailing into a perfect storm. You've worked decades to build a life of stability, and the fear of the five-year lookback rule or losing your homestead to medical bills is understandably exhausting. Learning how to protect assets from nursing home costs in Florida isn't just about financial planning; it's about ensuring your spouse isn't left stranded and your legacy remains intact for your children.

We believe that every senior deserves a safe harbor. This guide provides a clear roadmap to navigate these complex waters, showing you how to safeguard your savings and keep your family home secure despite rising long-term care expenses. We'll explore proven strategies to meet the $2,000 asset limit, explain how the $162,660 Community Spouse Resource Allowance works for those staying at home, and show you how specific tools like Fixed Indexed Annuities can help you reach a place of lasting peace of mind.

The Financial Storm: Understanding Nursing Home Costs in Florida

In 2026, the cost of a private room in a Florida nursing home averages $11,500 monthly. For many, this $138,700 annual bill feels like a leak in a ship that's impossible to plug. Long-term care isn't just medical treatment; it's the daily support needed for Activities of Daily Living (ADLs) like dressing, eating, or bathing. While many hope their health stays perfect, the reality is that 21% of Florida residents are over 65, and the demand for these services is rising rapidly.

You might assume that Medicare will act as your life jacket in this situation. It's a common misconception. Medicare only covers skilled nursing care for a limited 100-day window, and even then, you'll face a $217 daily co-payment after the first 20 days in 2026. Understanding Medicaid is the first step toward a more permanent solution. To better understand this concept, watch this helpful video:

Without a clear strategy for how to protect assets from nursing home costs in Florida, a lifetime of savings can vanish in less than two years. The spend-down trap occurs when a family is forced to pay for care out-of-pocket until they have almost nothing left. Florida Medicaid requires applicants to have no more than $2,000 in countable assets. This means that without professional guidance, you could be forced to liquidate everything you've worked for just to qualify for help.

Activities of Daily Living (ADLs) and Eligibility

Medicaid eligibility in Florida isn't just about your bank account. The Statewide Medicaid Managed Care Long-Term Care (SMMC-LTC) program requires a clinical evaluation to verify your level of care. You must typically demonstrate a need for assistance with several Activities of Daily Living, which include:

Bathing and personal hygiene

Dressing and grooming

Eating and nutritional support

Transferring and mobility

This assessment ensures that those with the highest clinical needs receive priority. It also creates a complex hurdle for families who are already under stress.

The Emotional Anchor: Why Proactive Planning Matters

Moving from a state of crisis to a position of protection is the best gift you can give your family. Proactive planning allows you to set the course before the storm hits. By focusing on senior financial planning in Palm Beach Gardens, you ensure that your spouse remains cared for and your legacy is preserved. This isn't just about numbers; it's about the peace of mind that comes from knowing your home and savings are safe.

Navigating the Medicaid Lookback and Florida Homestead Protections

Protecting your legacy requires a steady hand and a clear understanding of the currents in Florida law. One of the most significant challenges in learning how to protect assets from nursing home costs in Florida is the 60-month Medicaid lookback period. During this window, the state examines every financial transfer you've made. If you've gifted money or property to family members without receiving fair market value, you'll likely face a penalty. For 2026, Florida uses a penalty divisor of $10,645 to determine how long you must pay for care out-of-pocket before benefits begin. This makes the common strategy of "just giving it to the kids" a risky move that can leave you without a safety net when you need it most.

Your home remains your strongest shield in this journey. Florida offers robust homestead protections that keep your primary residence from being counted as a liquid asset. This protection stays in place even if you move into a facility, provided you sign a document expressing an "Intent to Return Home." In 2026, the Florida home equity limit for a single Medicaid applicant is $752,000. As long as your equity stays below this figure, your home is generally safe from being counted toward the $2,000 asset limit required for Medicaid coverage for nursing facilities.

Step-by-Step Asset Protection Framework

Distinguishing between exempt and countable assets is vital for success. Countable assets include cash, stocks, and secondary properties. However, exempt assets include your home, one vehicle, and personal effects. If your income exceeds the $2,982 monthly limit, a Qualified Income Trust, or Miller Trust, acts as a legal vessel to hold excess funds and maintain your eligibility. You can also utilize "spend-down" strategies, such as making necessary home improvements or purchasing a new vehicle, to lower your countable assets without triggering penalties.

If your estate includes a medical practice or care facility, it's important to recognize these as countable assets. Working with specialized firms like Healthcare Biz Brokers, Inc. can help you navigate the valuation and sale of such businesses to ensure they are integrated correctly into your long-term care plan.

The Danger of Unregulated Transfers

Attempting to navigate these rules without a plan is like sailing without a compass. Uncompensated transfers are viewed as a red flag by auditors, leading to long periods of ineligibility that can devastate a family's finances. Instead of risking your future on DIY transfers, consider more secure options like Personal Care Contracts or structured insurance products. If you're looking for a way to anchor your finances, you might find it helpful to connect with a professional guide who understands these local waters.

Building Your Safe Harbor: Proactive Financial Literacy and Insurance

True security comes from understanding that protection starts long before a nursing home application is filed. Reaching this stage of life is a milestone to celebrate, but it requires a sturdy hull for your financial ship. By integrating specific insurance and annuity products, you can create a robust defense against healthcare inflation and market volatility. Learning how to protect assets from nursing home costs in Florida means shifting your perspective from merely "spending down" to strategically positioning your wealth for long-term safety.

Leveraging Annuities for Medicaid Compliance

Fixed Indexed Annuities serve as a powerful financial anchor for many families. In Florida, these tools can help convert "countable" cash into a stream of "non-countable" income. This is particularly beneficial for Palm Beach Gardens residents looking to protect a community spouse. In 2026, the non-applicant spouse can retain a Community Spouse Resource Allowance of up to $162,660. By utilizing Medicaid-compliant annuities, you can ensure the spouse staying at home has the resources they need while the applicant qualifies for assistance. These are essential strategies to protect your assets from being depleted by monthly facility bills.

Living Benefits: The Modern Alternative to LTC Insurance

Traditional long-term care insurance is becoming increasingly difficult to find and maintain. Many seniors now turn to Life Insurance with Living Benefits as a more flexible alternative. These modern policies allow you to access a portion of your death benefit while you're still alive to cover chronic illness or nursing care. It's a way to ensure your premiums provide value whether you need care or simply want to leave a legacy. You can see how these tools fit into a broader Florida retirement guide to maximize your long-term stability. If you're ready to explore how these options apply to your specific situation, I encourage you to connect with Dennis Richards for a personalized assessment of your protection needs.

Charting Your Course to Long-Term Security

Navigating the complexities of Florida's long-term care landscape doesn't have to be a solo voyage. You've seen how the state's robust homestead laws and specific equity limits provide a foundation for safety. By understanding the 60-month lookback period and embracing modern tools like Fixed Indexed Annuities or Life Insurance with Living Benefits, you can secure a future that protects both your spouse and your children's inheritance. Mastering how to protect assets from nursing home costs in Florida is about replacing uncertainty with a clear, actionable roadmap.

Our team in Palm Beach Gardens provides the local expertise needed to handle intricate Medicaid rules with precision and care. We specialize in creating personalized strategies that act as a financial refuge for your hard-earned savings. Whether you're interested in living benefits or income-generating annuities, we're here to serve as your steady guide. We prioritize your family's well-being above all else, ensuring every detail is handled with integrity.

Your peace of mind is the ultimate destination. Let's work together to ensure your retirement years remain a time of celebration and stability.

Common Questions About Florida Asset Protection

Can the nursing home take my house in Florida?

No, a nursing home cannot directly take your home, and Florida's homestead laws provide some of the strongest protections in the country. For 2026, your primary residence is considered an exempt asset as long as your equity is below $752,000 and you or a spouse intend to return home. While the home is safe during your lifetime, proactive planning is still necessary to prevent the state from seeking estate recovery after you pass away.

What is the Medicaid 5-year lookback rule in Florida for 2026?

The lookback rule is a 60-month period where the state reviews your financial records to ensure you haven't gifted assets to qualify for assistance. If you transferred property or cash for less than its fair market value during this window, a penalty period is triggered. In 2026, the state uses a penalty divisor of $10,645. This means every $10,645 gifted results in one month where you must pay for care out-of-pocket.

How much money can a single person keep and still qualify for Florida Medicaid?

A single applicant is limited to just $2,000 in countable assets to qualify for long-term care benefits. This strict limit is why many families feel overwhelmed when researching how to protect assets from nursing home costs in Florida. It's important to remember that this limit only applies to "countable" assets like cash and stocks. Your home, one vehicle, and personal belongings generally don't count toward this $2,000 threshold.

What are the best ways to protect my parents' assets if they are already in a nursing home?

Even if your parents are already receiving care, crisis planning strategies can still safeguard their legacy. You can implement a legal spend-down by paying for home improvements on their exempt residence or purchasing a prepaid funeral contract. If their monthly income exceeds $2,982, a Qualified Income Trust is a vital tool to maintain eligibility. Medicaid-compliant annuities can also be used to transform countable savings into a protected income stream for a spouse remaining at home.

Comments